- European Medicines Agency approves first two pegfilgrastim biosimilars and another adalimumab biosimilar

- Pfizer launches NivestymTM, a filgrastim biosimilar, in the United States

- Only five of twelve approved biosimilars have launched in the United States

As pharmaceutical drug costs attract increasing media attention and political scrutiny, a growing number of biosimilar drugs are set to enter the U.S. and European markets in the coming years. Global sales for the top ten branded biologic drugs totaled approximately $71 billion in 2017[1]. Competition in the heavily regulated marketplace for these blockbuster therapeutics is expected to substantially impact the pharmaceutical industry and national health systems. To date, the U.S. has considerably lagged behind Europe’s expansion of biosimilar drug options. The RAND Corporation estimates that biosimilar products can save the U.S. health system approximately $54 billion over the next decade, as discussed here.

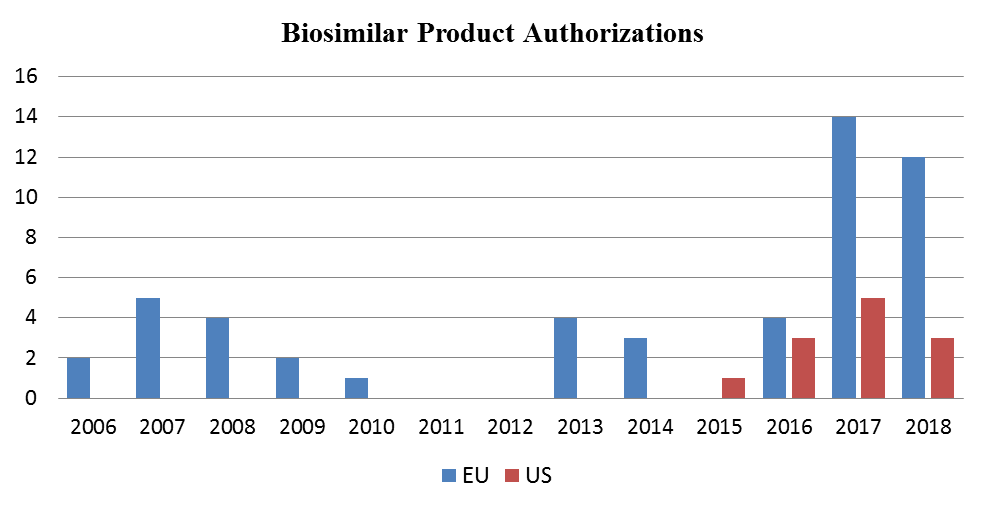

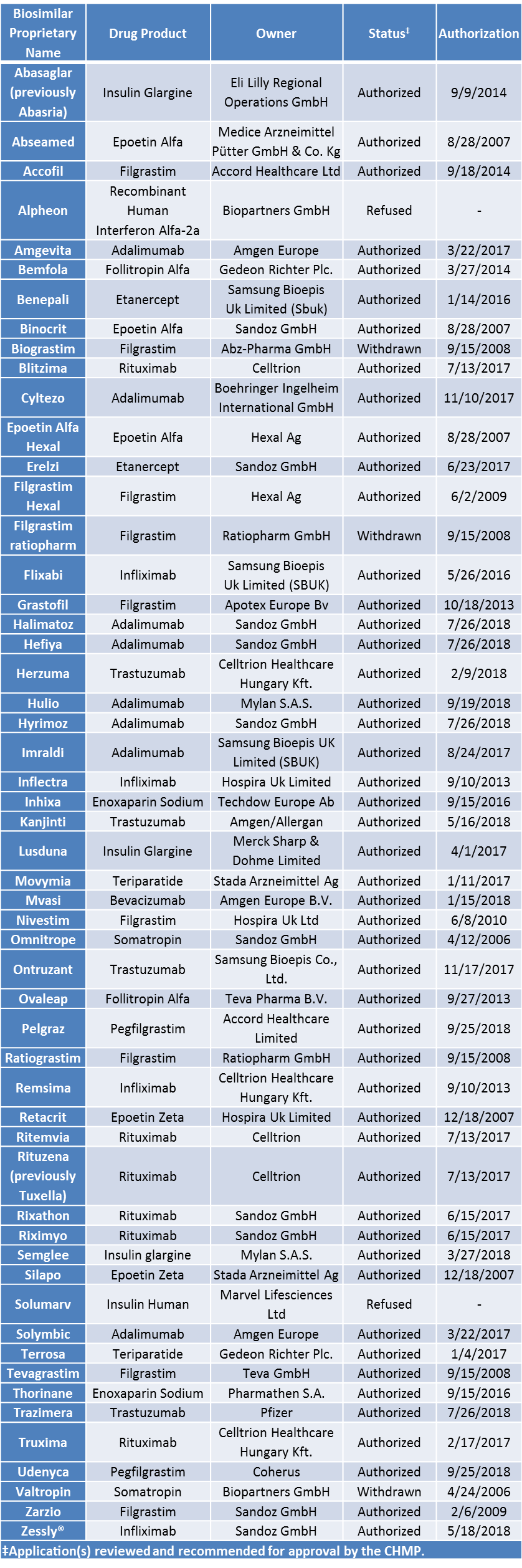

Since 2005, the biosimilar regulatory framework in Europe has been implemented through the Committee for Medicinal Products for Human Use (CHMP) under the European Medicines Agency (EMA). The CHMP provides initial assessments for marketing authorization of new medicines that are ultimately approved centrally by the EMA. Since Sandoz’s somatotropin biosimilar Omnitrope® was first authorized on April 12, 2006, an additional 48 out of 53 applications have been approved in Europe. Three of the authorizations have been withdrawn post-approval by the marketing authorization holders (Table 1).

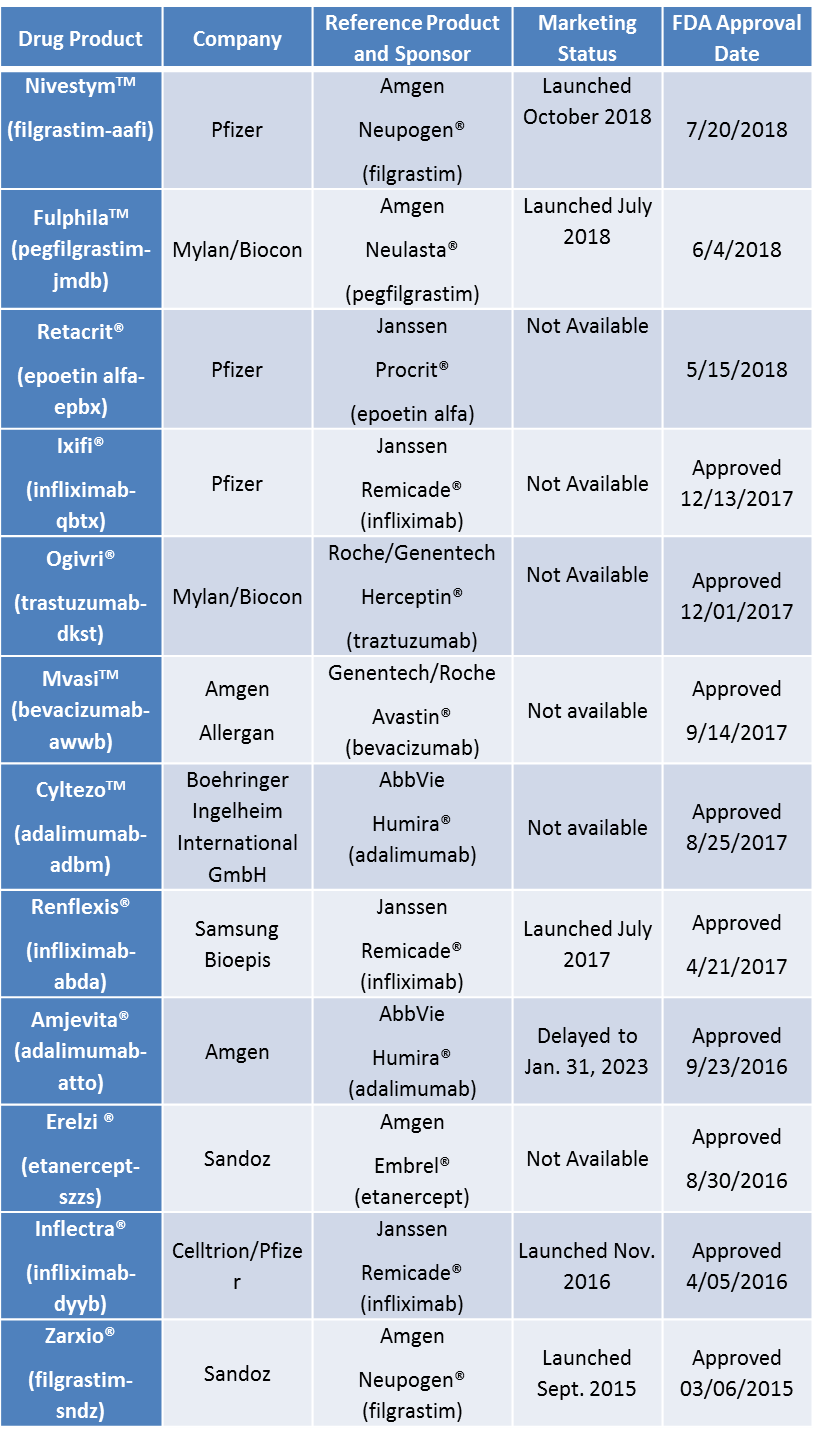

The U.S. did not implement a regulatory framework for biosimilar evaluation until after enactment of the Biologics Price Competition and Innovation Act (BPCIA) of 2009. Given that the first U.S. biosimilar drug was approved almost a decade after the first in Europe, the number of authorized biosimilar drugs in Europe far exceeds the number of biosimilars approved in the United States. Sandoz’s filgrastim biosimilar Zarxio® received the first U.S. approval in 2015, whereas nine filgrastim biosimilars have been approved in Europe dating back to multiple authorizations in 2008. Zarxio® (in the U.S.) and Zarzio® (in Europe) are biosimilar to the reference product Neupogen® marketed by Amgen and originally licensed in 1991. Subsequent to Zarxio®’s approval, only eleven other biosimilar drugs have gained U.S. approval to date (Table 2). As illustrated in the following graph, while the EU’s significant head start led to an imbalance in the number of biosimilar drugs available in the respective markets, the EU’s relatively higher rate of approvals in recent years has widened its lead over the United States.

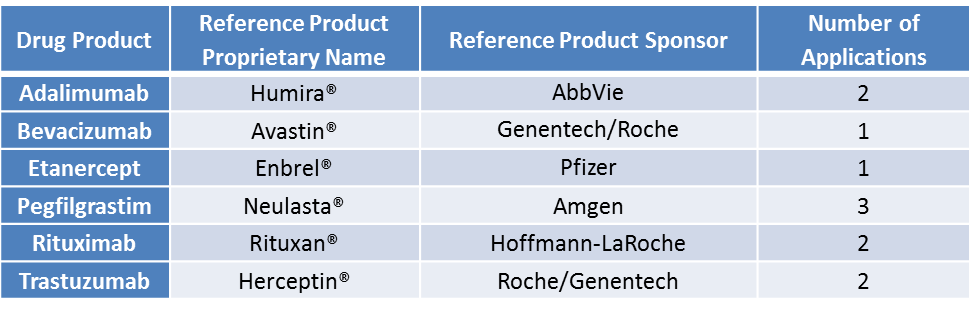

Currently, eleven biosimilar applications are under review by the EMA for marketing authorization (Table 3). As an increasing number of patents expire on blockbuster biologic drugs, the number of abbreviated biologics license applications is also increasing. Biosimilars for at least twelve different original biologics are currently navigating the United States Food & Drug Administration’s (FDA’s) biosimilar pathway or are in late stage development (Table 4).

On September 19, 2018, the EMA approved Hulio®, another biosimilar to Abbvie’s Humira® in Europe. On October 17, 2018, upon expiration of a European patent covering Abbvie’s Humira®, several biosimilar adalimumab products that had been previously authorized by the EMA launched in Europe including Novartis’ Hyrimoz, Amgen’s Amgevita, Biogen’s Imraldi, and Mylan and Fujifilm’s Hulio.

On September 25, 2018, the EMA approved Coherus’ UdenycaTM and Accord Healthcare’s Pelgraz®, the first pegfilgrastim biosimilars to Amgen’s Neulasta® in Europe.

On October 11, 2018, Celltrion and Teva announced that the FDA Oncologic Drugs Advisory Committee voted unanimously to recommend approval of CT-P10, a proposed monoclonal antibody (mAb) biosimilar to Roche’s Rituxan® (rituximab).

Given biosimilar applicant experience in navigating the EMA process and the EMA’s high authorization rate, the FDA will need to continue to provide useful guidance and streamline the approval process in order to reduce the imbalance.

Table 1. European Medicines Agency List of Approved Biosimilar Drugs (updated October 19, 2018).

Table 2. U.S. Food and Drug Administration List of Approved Biosimilar Drugs (CDER list of licensed biologics updated on October 22, 2018).

Table 3. European Medicines Agency List of Biosimilars Under Evaluation for Marketing Approval (Source: EMA list of applications for new human medicines updated on September 28, 2018).

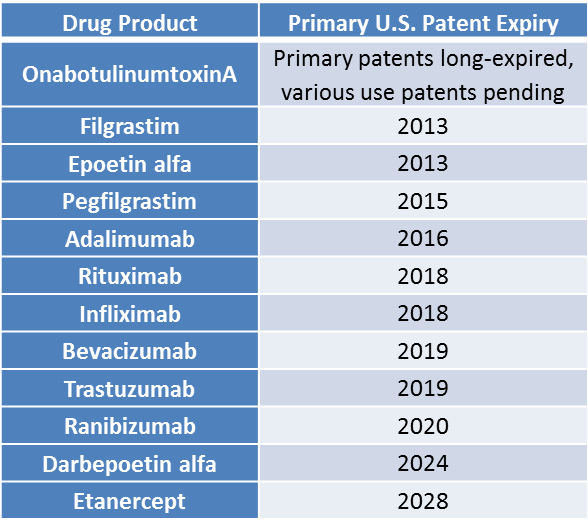

Table 4. Biologics having already expired or nearing primary patent expiry in the U.S. that have biosimilars in the regulatory pipeline.

[1] Based on sales reported by respective manufacturers (1. Humira—Abbvie, 2. Rituxan—Roche, 3. Enbrel—Pfizer/Amgen, 4. Herceptin—Roche, 5. Avastin—Roche, 6. Remicade—Johnson & Johnson/Merck, 7. Lantus—Sanofi, 8. Neulasta—Amgen, 9. Avonex—Biogen, 10. Lucentis—Roche/Novartis).